No further delay, click the link below to get your USD 8 now adn share it to your social media to get USD 8 each of your friend open the red packet! Hurry! Event ends on 17 February 2016!

Get your first USD 8 here and more!

Sunday, January 29, 2017

Saturday, December 17, 2016

A New Financial Strategy Game - TAGG (earn-as-you-play)

We talking about casual games, like Clash of clans, Candy crush, Angry Birds, Final Fantasy Mobius, Ingress, and many other pay-to-win or pay-to-play MMO strategy games.

10? 20? 50? Some may have spent thousands. Just look at those in top ranks.

What if I tell you that you can earn as much as around 20% from the money that you would have spent on these game. Attractive?

Today I want to share with you a new gaming-financial frontier - TAGG.

How many of you have heard this new fintech firm called Six Capital Investment? I bet not many of you know, in fact, I was lucky enough to discover this fintech pioneer.

Headquartered in Singapore, Six Capital is a movement that specializes in the field of financial technologies and machine intelligence. They have advised many high-end investor in the financial market, their service is not an average investor like you or me can afford.

Six Capital imagined a world where games were no longer dismissed as a waste of time - but a platform where casual gamers could earn-as-they-play in a manner that was not overly complex and time-consuming.

Thus, they developed TAGG.

TAGG is an evolving strategy battle card game powered by Six Capital’s fintech engine - Ricebowl, which stabilises and maintains its in-game economy. Through the direct monetisation of in-game purchases, TAGG translates value created back to the gamers, enabling them to earn as they play.

Ricebowl also adopts a man-machine hybrid approach towards engaging the financial markets in a non-speculative manner, recognising data as the rising asset class.

Six Capital together with various co-creation partners such as -

- MIT Media Lab in the U.S.,

- Universitas Gajah Mada and Binus University in Indonesia,

- Singapore Institute of Management Global Education,

- Chartered Banker’s Institute of the UK,

- People’s Bank of China,

- China Centre for Financial Trading (CCFT),

- CNBC,

- The Wall Street Journal (WSJ), and

- AirAsia.

TAGG as a new product of Six Capital, main purpose is to bring the wealth and health to the bottom, has organised many in-game event throughout the year -

Ok, that should be good for the introduction. Now back to the main thing - How much you have spent on purchase of in-game items? and how much you can earn from it?

I have been with TAGG for almost 10 monhts, here is my result -

Invested: USD 420

Income generated: USD 93

Yield: 22%

What's more, Six Capital even guarantee your capital and positive returns for every period.

Impressive hu? I say this is the power of crowd, data and machine. All these income was accumulated from micro transaction done by the Ricebowl. I do get about USD 10 for every month!

Currently there is a faction war in TAGG between Ironforge and Ravenclaw. Join me at Ironforge! Together, we can achieve greater yield boost!

Share this article or this link to your friends so that we can dominate the other faction

https://goo.gl/Y4Msz8

Friday, December 16, 2016

5 most popular KLSE listed banks - 10 years summary outlooks

On the historical average, 2018 or so is looking dangerous. Will the market soon to have its major correction? Have you think about the opportunity that always tag along with every crisis?

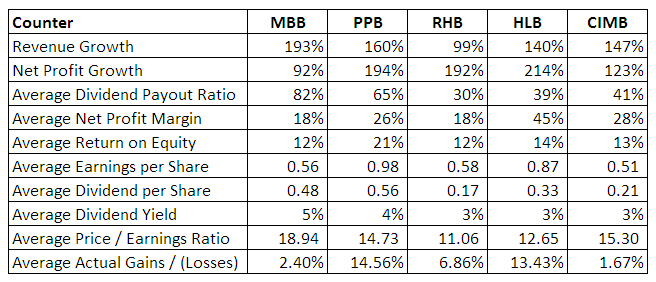

Today, I've pull out some data from stock market for a 10 years summary of the 5 most popular banking stock in Bursa Malaysia (KLSE).

There are -

Today, I've pull out some data from stock market for a 10 years summary of the 5 most popular banking stock in Bursa Malaysia (KLSE).

There are -

- CIMB Group Holdings Berhad

- Hong Leong Bank Bhd

- Malayan Banking Bhd

- Public Bank Bhd

- RHB Capital Bhd

Based on the summary, Maybank has the highest 10-years revenue growth compared to the other 5 banks, however it only achieved an average 18% of net profit margin. If you have follow the quarterly reports of these banks, you will noted that Maybank has the highest revenue of RM44 Billion, in terms of numbers, compared to Public Bank who only have about RM20 Billion in revenue, Maybank does not did very well in these years, in fact, its latest TTM of net profit margin is only 14%, which is the lowest of the 10-years period. However, good news is Maybank has recently taking some cost efficiency improvement, we hope this will bring benefits to its profit margin in the near future.

Although, no doubt that Public Bank is the strongest banking counter in KLSE, closed at RM19.80 on 16 Dec, it has almost won all the readings of the average 10-years period - return of equity, earnings per share and dividend per share, but let's not jump into conclusion so fast, after all, you won't make significant gains from such an, established stock, higher gains always come with higher risk, remember?

My favorite from the 10-years data is Hong Leong Bank. Hong Leong Bank quietly defending its territory in these painful.. err.. nope, I will say a very competitive 10-years period. It is very resilient. Hong Leong Bank has a very stable profit margin similar to the Public Bank's, but in a more profitable way. In the 10-years period, Hong Leong Bank has achieved an average of 45% of net profit margin, surpassed Public Bank in terms of net profit growth. Speaking of net profit growth, RHB Bank performed well, raking 3rd with close proximity with Public Bank.

The most generous bank? No one can match with Maybank. Commanding the largest market capitalisation (well, I know Public Bank has recently overtook Maybank, but since we are discussing the 10-years period, please bear with me), the with a very huge cash pile, Maybank is able to achieved an average of 82% of dividend payout ratio, very closed to REITs counters! Downside is, its share price did not growth very well.

On price-per-earnings ratio, Public Bank, RHB Bank and Hong Leong Bank seem able to make their stands well Maybank and CIMB Bank are not. Speaking of CIMB Bank, what it actually offer that making its being scope in for the 10-years summary? Because of its relationship with the house-in-charge? Hmm.. I don't know, maybe, who's know? For now let's see.

Ok, now you may wonder, what is the actual gains/losses means? Well it is certainly not my gains/losses during these 10-years, I wish it is, but too bad it's not.

The actual gains/losses are the combined average gains/losses calculated from dividend and increases in share price, meaning, revenue and capital gains. In simple way of explanation, if you invested 10 years ago in all these 5 banks, these are the gains/losses from your initial capital. I've ignored all sorts of present value, discounting valuation, capital reinvest, etc. These are just too complicated for me, perhaps you can help me to sort out, drop me a message if you do.

So, my strategy is to use Public Bank as a base since it is the most stable counter, and add an extra layer on Hong Leong Bank, finally accumulate some Maybank if the price is attractive.

How about your strategy?

Disclaimer: This is not an investment advice nor buy calls or or sell calls. You are not advised to make investment in the stocks mentioned in this article, or any articles that appeared in this website, blog or posted by me, by merely based on the information discussed in the aforementioned. You are advised to do you own research before invest in any stock.

Subscribe to:

Posts (Atom)